2025 Manufacturing Industry Outlook

Deloitte

By John Coykendall, Kate Hardin, John Morehouse

20 Nov, 2024

Manufacturers prioritize targeted investments in their digital and data foundation to boost innovation and tackle ongoing skills gap and supply chain challenges

In 2024, US manufacturing experienced continued investment even as higher interest rates and a challenging business environment have created obstacles to near-term industry growth. Deloitte’s analysis of S&P Global data reveals that while 2024 began with the manufacturing purchasing managers’ index (PMI) moving into expansion for the first time since April 2023, which continued for the first half of the year, weaker demand nudged the PMI back into contraction in July 2024. In addition, the November 2024 PMI report identified an ongoing combination of falling orders and rising customer inventories, which could signal the need for manufacturers to further cut production in the coming months. While the rate of inflation has diminished, manufacturers continue to face higher costs: The producer price index for input materials and components seems to have stabilized but remains high, while total compensation, which includes wages and benefits, has continued its upward climb.

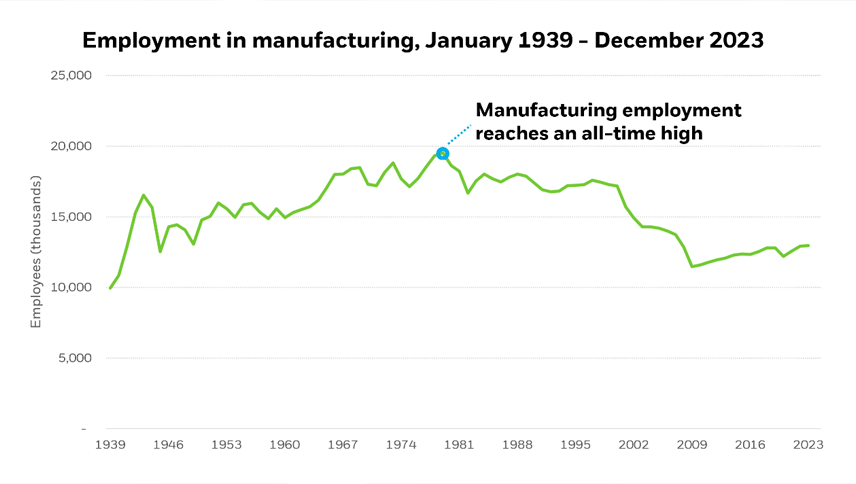

Meanwhile, weaker demand due in part to the challenging business climate and higher interest rates may have helped to ease talent and supply chain pressures. Data from the US Bureau of Labor Statistics indicates that the labor market has continued to stabilize through 2024 as quits, hires, and job openings in manufacturing have steadily declined, and employment has leveled off at around 13 million as production levels have stabilized. However, talent challenges persist. Even as labor markets have loosened, nearly 60% of manufacturers in the National Association of Manufacturers (NAM) outlook survey for the third quarter of 2024 cited the inability to attract and retain employees as their top challenge. Supply chains have also improved, with the average delivery time for raw materials dropping to 81 days by October 2024, representing a 2% year-over-year decline. However, they still have not returned to pre-pandemic norms.

At the same time, 2024 demonstrated continued, albeit cooling, investment in US manufacturing that could lead to longer-term growth. For instance, a total of more than US$31 billion in investment in 192 clean-technology-manufacturing facilities has been announced during the year through October, and these investments are expected to create close to 27,000 new jobs. Construction spending in manufacturing—that is, dollars invested to build new or expand existing manufacturing facilities—reached a new record of US$238 billion in June 2024, and this is also likely to continue to spur investment in new equipment and intellectual property. However, the year-over-year pace of growth slowed from 41.3% in September 2023 to 20.5% in September 2024.

Looking ahead to 2025, manufacturers are expected to continue to face a challenging and uncertain business climate due to a combination of higher costs, potential policy changes following the US and global elections, and geopolitical uncertainty. Surveyed manufacturers in NAM’s 2024 third-quarter outlook expect raw material and other input costs to grow by 2.7% over the next 12 months. However, lower interest rates have the potential to fuel investment and business and consumer spending, which could spark higher demand for manufactured goods. On the other hand, while the Federal Reserve has expressed confidence that it can achieve a “soft landing,” there is still a risk that the recent cooling in the labor market could accelerate, potentially leading to an economic slowdown. For instance, consumer spending has remained relatively robust through September 2024, but this could slow in 2025 if unemployment accelerates, which might affect the manufacturing industry.

Potential policy changes after the 2024 US elections, as well as elections across the globe, may have impacts on supply chains, demand, and long-term investment in manufacturing. Changes to trade policy and tariffs could drive up raw material and component costs and could have ripple effects throughout the supply chain. Potential adjustments to parts of the Inflation Reduction Act could impact investment in certain aspects of clean technology manufacturing in the United States.

Deloitte’s 2025 Manufacturing Industry Outlook explores the following trends to help leaders shape strategies and priorities in the coming year:

- Talent: Positioning for renewed demand and maintaining a long-term workforce strategy

- Artificial intelligence and generative AI in manufacturing: Prioritizing targeted, high-ROI investments

- Supply chain: Tackling disruptions and elevated costs with agility and efficiency

- Smart operations: Building the foundation while prioritizing high-value projects

- Clean technology manufacturing: Moving ahead strategically amid uncertainty

1. Talent: Positioning for renewed demand and maintaining a long-term workforce strategy

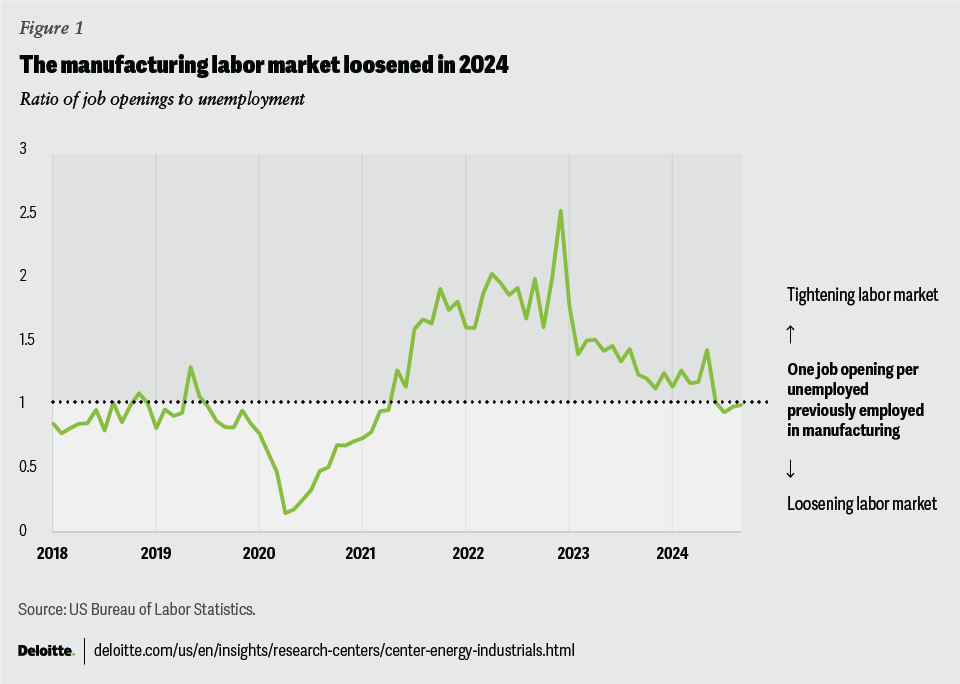

Labor market tightness in the manufacturing industry has been declining in 2024, and, in fact, July was the first month since May 2021 that the number of unemployed in manufacturing exceeded the number of job openings (figure 1). The quits rate in manufacturing reached 1.6% in September 2024, marking a 0.2 percentage point drop since January 2024. Weakening demand for manufactured goods and labor market loosening seems to have created a better balance, at least in the near term, between labor supply and demand in manufacturing.

However, talent challenges are still salient. The Employment Cost Index for total compensation in manufacturing, which includes employee wages and benefits, has continued to climb in 2024, gaining 3.8% year over year as of September. Labor participation rates have been declining in the United States for over two decades, due in part to an aging population, and this may continue through at least 2030. Challenges such as workers’ access to child care, reliable transportation, and their desire for flexibility also remain. A study conducted by Deloitte and The Manufacturing Institute in 2024 showed that 1.9 million manufacturing jobs could go unfilled over the next 10 years if talent challenges are not addressed. The study also found that roles that require higher-level skills could grow the fastest between 2022 and 2032, and that a combination of technical manufacturing, digital, and soft skills will likely be required.

Favorable economic conditions in 2025 such as lower interest rates and continued investment in US manufacturing may reignite demand in the industry, which could intensify labor shortages. Though wages are likely to continue to rise, manufacturers have a cost lever that they can pull: reducing turnover. According to a 2024 survey of more than 300 human resources leaders at US manufacturing companies conducted by the UKG Workforce Institute, 60% of respondents indicate that the average cost to replace one skilled frontline worker ranges from US$10,000 to US$40,000, while 56% say that employee turnover has a moderate to severe impact on their bottom-line finances.

To help meet workers’ changing expectations, reduce turnover, and plan for demand volatility, companies seem to be increasingly focusing on improving the worker experience, taking an ecosystem approach to talent development, and leveraging digital tools that offer advanced talent planning and workforce management capabilities. A recent report by Gartner suggests that by 2025 over 80% of large businesses that have hourly employees will have invested in advanced workforce management software solutions. In addition to supporting broader digital initiatives to improve operational efficiency, a key goal of these investments is to improve the worker experience, including capturing employee sentiment, suggesting adjustments to shift patterns, enabling flexible scheduling, and improving company communication with hourly workers, according to the report.

The study also indicates that by 2030, AI-based management of employee skills and how people are deployed to meet business needs will be a core capability. By tracking and connecting important parameters like employee skills and certifications (that is, using a skills matrix), the number of people and skills required to produce certain products, and accurate demand forecasts, these tools could allow companies to efficiently plan for the specific workforce needed for upcoming production runs. If gaps are identified, companies could offer upskilling opportunities for existing employees, which can increase retention, or work within the talent ecosystem to find and develop workers with the requisite skills.

Taking this approach could also enable tailored upskilling that helps prepare employees for future work, for example, working alongside advanced technology such as gen AI. Advanced talent-planning tools can also support manufacturers taking a skills-based approach, which may be increasingly important for broadening the talent pool. These investments and a focus on long-term talent strategies may help manufacturers build and retain a skilled workforce for 2025 and beyond.

2. AI and generative AI in manufacturing: Prioritizing targeted, high-ROI investments

As the enthusiasm surrounding gen AI shifts from “…unbridled excitement” to “a more nuanced and critical evaluation of its real impact on business outcomes,” manufacturers have already made significant investments in AI and gen AI, and this trend is expected to continue in 2025 and beyond. Deloitte’s 2024 Future of the Digital Customer Experience survey found that 55% of surveyed industrial product manufacturers are already leveraging gen AI tools in their operations, and over 40% plan to increase investment in AI and machine learning over the next three years. However, companies seem to be taking a more measured approach toward gen AI and AI implementation by following their traditional, holistic return on investment processes. A 2024 survey of manufacturers by the Manufacturing Leadership Council found that 78% of respondents indicate that their AI initiatives are part of the company’s overall digital transformation strategy. And, as is typically the case with technology investments, a primary measure of success for gen AI will be its ability to drive value in the organization.

A prerequisite for AI adoption is access to quality data, and companies seem to be shifting their focus in this direction: Three-quarters of respondents in a recent Deloitte survey indicated that their organization has increased investment around data life cycle management to support their generative AI strategy. However, challenges still exist—in another survey, nearly 70% of manufacturers indicated that problems with data, including data quality, contextualization, and validation, are the most significant obstacles to AI implementation. To help overcome these challenges and maximize ROI, manufacturers might consider starting with use cases where there is already a strong data foundation in place.

One example is customer service applications, which are often digital and language-based, and offer access to a wealth of data that typically doesn’t require significant data harmonization or modernization, such as call records, technical documents, warranty data, and claims information. In fact, 74% of surveyed manufacturers in Deloitte’s 2024 Future of the Digital Customer Experience survey indicated that they plan to use or are already using gen AI to enhance their customer experience. Example use cases include gen AI–based virtual chatbots that can allow customers to efficiently evaluate product specifications and features during their buying journey, or gen AI–based service manuals combined with augmented reality that can facilitate rapid and efficient remote assistance for maintenance and repair.

Another example is product design. For instance, according to data provider IDC, by 2028, the demand for product innovation will drive 50% of large manufacturers to evaluate engineering archives using generative AI to uncover new opportunities for innovation on legacy products. Tying the use cases to critical business initiatives or priorities, such as enhancing customer experience or product innovation, can also be important for securing internal funding and support.

Identifying targeted opportunities to invest in AI, including gen AI, may be key for manufacturers in 2025 as elevated costs and uncertainty are expected to continue in the coming year. Improved efficiency, productivity, and cost reduction have been identified as important benefits achieved through generative AI implementation. In addition, in a recent survey, manufacturers indicated that AI and machine learning have the largest impact on business outcomes relative to other smart manufacturing technologies, and that gen AI or causal AI offer the largest ROI behind cloud and software-as-a-service technologies. To support AI use case implementation in 2025 and lay the groundwork for the future, it will be important for manufacturers to focus on building an overall AI and data strategy, including establishing an operating model, setting up governance, and identifying risks. Yet in a 2024 survey by the Manufacturing Leadership Council, only 51.6% of manufacturers indicated that they have a corporate AI strategy. A dedicated focus on organizing and structuring data will also be important to create the foundation to facilitate long-term investments in AI and gen AI.

3. Supply chain: Tackling disruptions and elevated costs with agility and efficiency

Supply chain challenges have eased since the height of the COVID-19 pandemic, but pressures remain. For instance, average lead times for production materials have shown significant improvement since their peak in 2022 but remain stubbornly higher than pre-pandemic levels. While global supply chain disruptions persist, such as attacks on container vessels in the Red Sea, costs also remain high. Over 35% of surveyed manufacturers cited transportation and logistics costs as a primary business challenge in the third quarter of 2024.

In 2025, companies are expected to face continued supply chain risks, disruptions, potential delays, and elevated costs due to several contributing factors:

- Shipping delays: Geopolitical tensions and additional factors may contribute to ongoing shipping challenges in 2025. For example, route changes in response to Houthi militia attacks on cargo containers in the Red Sea are likely to continue. The increased transit time on these routes has impacted shipping capacity across the globe since the attacks began in October 2023, causing significant delays and shipping rates to double by the summer of 2024. Starting in 2023, low water levels in the Panama Canal due to drought caused delivery delays and rising costs for goods and raw materials between the United States and Asia, as well as additional global routes. The drought has subsided and low-water-level restrictions have eased in 2024, with the average number of daily trips through the canal approaching pre-drought levels as of August. However, drought conditions could return.

- Labor challenges throughout the value chain: Ongoing labor shortages from production to transportation to warehousing could contribute to delays and higher costs throughout the value chain in 2025. The shortage of truck drivers in the United States continues and is expected to accelerate in the years ahead. In a 2024 survey of more than 600 manufacturing professionals, over 80% said that labor turnover had disrupted production, which can lead to slower deliveries. Labor turmoil in supply chains is also a growing challenge across the globe. For example, while the October 2024 strike by US dockworkers on the East and Gulf Coasts was resolved in just three days, supply chains were impacted and the worker contract expires on January 15, which could potentially lead to additional disruptions in 2025.

- Rising input costs: According to the NAM third-quarter 2024 outlook survey, respondents expect both wages and raw material prices to continue to rise by another 2.7% over the next 12 months.

- Potential government policy changes following US and global elections: 2024 was considered a “super year” for elections with 72 countries going to the polls and approximately 3.7 billion people—nearly half of the world’s population— potentially voting, according to the United Nations. Governmental changes and ensuing policy changes can affect global supply chains due to a number of factors, including geopolitical tensions, trade, tariffs, and industrial policy. For instance, changes to government policy could bolster supply chain restructuring efforts to balance cost and resilience, such as the nearshoring activity that has led Mexico to become the leading trade partner for the United States. Respondents in the 2024 Fortune/Deloitte CEO survey indicated international trade as the third top area where US elections could have the greatest impact, behind regulations and taxes. And manufacturers may already be bracing for potential changes: According to the NAM 2024 outlook surveys, the proportion of manufacturers citing trade uncertainties (such as actual or proposed tariffs) as a primary business challenge increased sharply to 34.3% in the second quarter from 25.8% in the first quarter, and continued to rise to 36.8% in the third quarter.

As supply chain pressures have abated since the COVID-19 pandemic, companies have shifted their strategy from a primary focus on resilience to a new emphasis on balancing optimized cost and resilience. Techniques such as diversifying sources, pursuing mergers and acquisitions, enhancing partnerships, and building internal capabilities are helping some companies achieve this goal. Amid the disruptions and high costs that could characterize supply chains in 2025, these approaches are likely to remain important.

Staying focused on investment in digital tools that enable advanced supply chain planning techniques, better collaboration with suppliers, simulation, and enhanced visibility may provide an additional boost. In a recent study, 78% of manufacturers indicated that they have implemented or are planning to invest in supply chain planning software. Respondents also ranked this software fifth out of 10 technologies that drive the most significant ROI. According to another 2024 report, some of the top trends expected to impact industrial product manufacturers’ supply chains by 2027 are big data and advanced analytics, supply chain digitization, and data management. The top priority for sourcing and procurement in 2024 for all companies surveyed (across industries) was implementing new technologies and capabilities, and this trend is likely to continue in 2025.

4. Smart operations: Building the foundation while prioritizing high-value projects

Manufacturers have continued investing in digital technologies over the last several years despite economic uncertainty, rising costs, and a challenging business climate. For instance, Deloitte’s Digital Maturity Index 2023 survey found that 98% of 800 surveyed manufacturers in four major global economic regions have started their digital transformation journey, compared with 78% in 2019, and respondents reported cost optimization, operational efficiency, product innovation, and improving customer experience as key drivers for the shift. Further analysis showed that technology investments made by manufacturing companies accounted for 30% of their operating budget in 2024, compared with 23% in 2023, with cloud, gen AI, and 5G being the top three technologies with the greatest ROI.

Given the need to address elevated material and labor costs, an ongoing skills gap, and potential disruptions from geopolitical factors, investments in digital technologies across manufacturing organizations—in other words, the push toward smart operations—is likely to continue in 2025.

Falling interest rates and the potential for growth could even accelerate investment. Manufacturers will likely continue to prioritize investments in their digital core and data foundation that can enable targeted, high-ROI use cases for cutting-edge technologies such as AI, gen AI, and extended reality (XR). Investments in the following technologies and systems are likely:

- Manufacturing operations management and manufacturing execution systems can connect the enterprise to the shop floor and provide visibility into data across the organization.

- The Unified Namespace data architecture strategy can provide a central source of real-time standardized data that can be utilized by a variety of systems across the business. Unified Namespace can eliminate the need for complicated direct connections between disparate systems that often create significant interoperability challenges. It may also lay the foundation for software-defined manufacturing, which aims to further simplify how new technologies are integrated into manufacturing environments in the future.

- 5G technologies support data collection and communication: According to Deloitte’s 2024 Future of the Digital Customer Experience survey, 34% of industrial product manufacturers plan to invest in 5G technology over the next one to three years.

- The model-based enterprise can support the digital thread: One in five (21%) of industrial product manufacturers plan to invest in model-based enterprise over the next one to three years.

- XR and AI may help meet ongoing needs like efficient workforce training, retaining the knowledge of retirees, and augmenting human capabilities. Nearly 30% of industrial product manufacturers plan to invest in XR technologies over the next one to three years, while more than 40% plan to invest in AI and machine learning.

The use of simulation in the manufacturing industry could also continue to grow, especially given the potential for business disruptions, the need to control costs, and the continued proliferation of AI tools. For example:

- Causal AI can be used to more effectively simulate cause-and-effect relationships, thereby enhancing decision-making capabilities.

- Production line simulation can help eliminate bottlenecks and optimize the workflow before any physical changes are made.

- Process simulation is the top use case that surveyed manufacturers implemented using metaverse technologies, according to the 2023 Deloitte and Manufacturing Leadership Council Industrial Metaverse Study, while factory simulation was also prevalent. Higher throughput and reduced costs were the primary benefits that companies gained from implementation.

- Business scenario simulation is also being employed by manufacturers. Using a model of the enterprise, challenges such as employee absences, raw materials that arrive with quality issues, and supply chain disruptions can be simulated, and potential actions can be identified to optimize the response.

Another trend to watch in 2025 is the likely continued evolution of manufacturing toward a software-driven industry—not just within the factory but also for connecting to products in the field—similar to what has occurred in the auto industry. According to the 2024 Future of the Digital Customer Experience study, industrial manufacturers are increasingly enhancing the digital connection to their products to gather usage and operational performance data that can help improve performance and serviceability. As one example, customers can access portals to monitor fleet performance, schedule maintenance, and chat with company representatives to resolve issues. Overcoming interoperability challenges between new and legacy systems, prioritizing cybersecurity and data protection, and developing talent with a blend of technical knowledge, digital skills, and soft skills are likely to be important factors for success in these efforts. They will also likely be key to supporting the broader evolution toward smart operations in 2025.

5. Clean technology manufacturing: Moving ahead strategically amid uncertainty

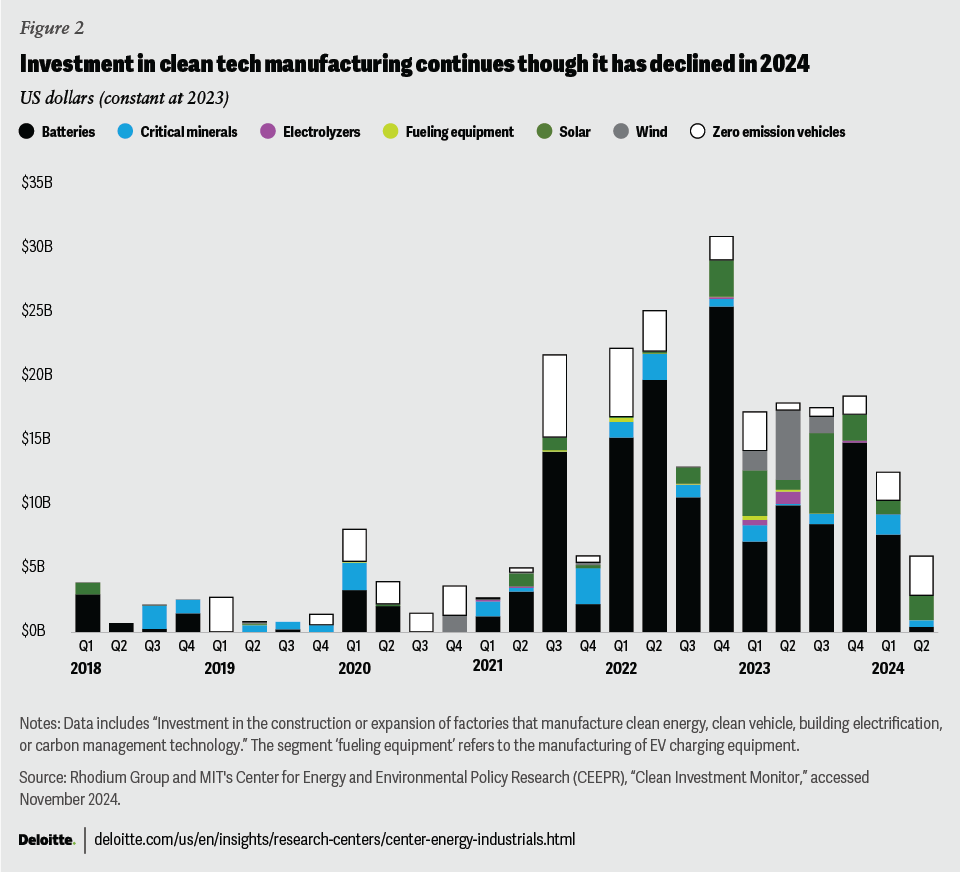

According to Deloitte’s analysis of Clean Investment Monitor data, significant investment in clean technology manufacturing has continued throughout 2024, but there has been a decline since 2023 (figure 2). In 2024, some automakers have also reduced investment in electric vehicles in response to slower-than-anticipated passenger electric vehicle adoption. For example, some companies’ goals to create 100% electric model lineups are stretching further into the future, while others are shifting toward hybrids for the models initially planned for 100% electrification.

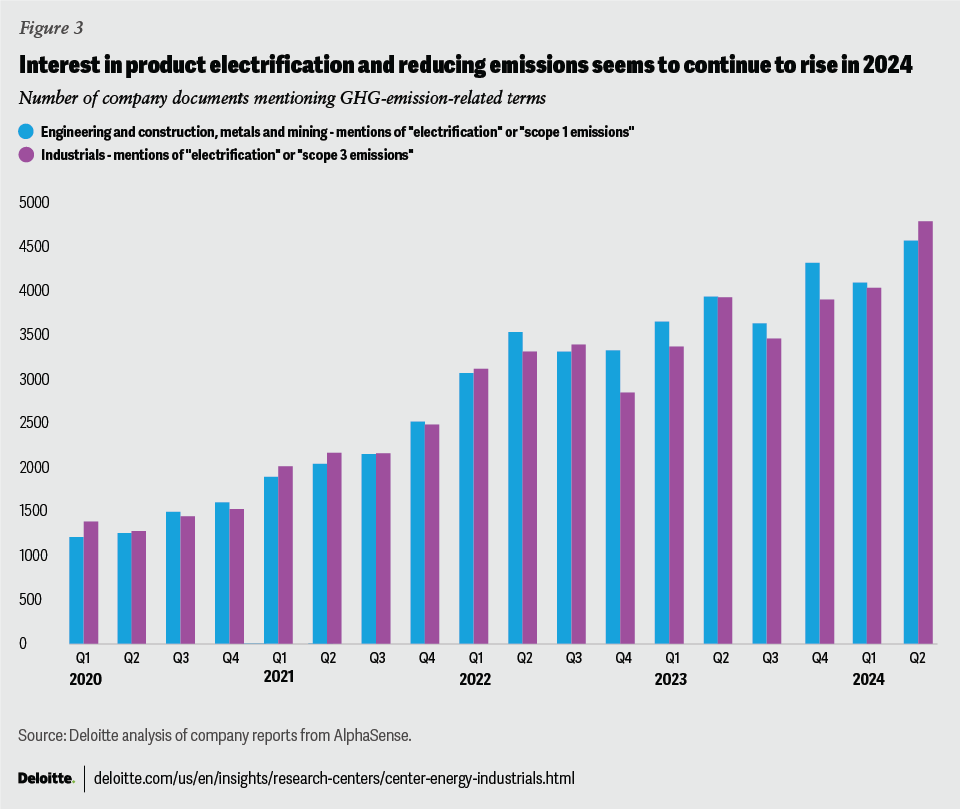

However, while overall investment in US clean technology manufacturing seems to have decelerated in 2024, Deloitte’s analysis of investor reports suggests a sustained commitment to electrification and decarbonization of products made by US industrial manufacturers, which aligns with their customers’ apparent continued focus on reducing operational emissions. The number of reports from industrial companies that mention “electrification” or “scope 3 emissions” has increased since January 2020 and has continued to rise in 2024 (figure 3). The same is true for company reports that mention either “electrification” or “scope 1 emissions” from the engineering and construction, and mining and metals industries, which often serve as customers to industrial manufacturers. The data suggest that industrial companies seem to be maintaining their focus on reducing the emissions of their products. The findings also suggest that customers seem to remain intent on lowering their operating emissions, which should continue to drive demand for lower-emission products.

According to Deloitte’s analysis of investor reports of several heavy equipment and engine manufacturers, some companies have continued to make cautious, targeted investments in adding lower-carbon options, such as electric and hydrogen power, to their product lines. They seem to be moving toward the goal of meeting previously set scope 3 emissions targets even in a challenging business climate. For example, one heavy equipment manufacturer plans to add over 20 electric and hybrid model options to its lineup by 2026.A diesel engine manufacturer reports that it continues to make progress on its 2030 goal for a 25% reduction in product lifetime greenhouse gas emissions (scope 3) from new products.

Customers of industrial product manufacturing companies also seem to be maintaining commitments to the adoption of clean technologies to meet their scope 1 emissions goals. For example, a strategic alliance has been formed to develop electric underground mining trucks, aiming for net-zero carbon emissions by 2050, and the first prototype was delivered to a mine for testing in October 2024.

Several suppliers to industrial product manufacturing companies continue to strategically transform their portfolios to align with electrification and reduced emission trends, according to Deloitte analysis of company reports. These companies are emphasizing electrification as part of their strategic focus, particularly in clean energy and sustainable solutions. Some companies are also expecting growth driven by electrification and the energy transition.

Though industrial product manufacturers seem steadfast in meeting company-imposed emissions goals for their products, looking ahead to 2025, there are several factors that could potentially impact further investment in the development and delivery of clean technology products.

- Government incentives and regulatory policy: With the possibility of policy and regulatory changes following the US elections, companies may employ a “wait and see” approach in 2025. In fact, regulations and taxes were tied as the top factors surrounding the US elections that could impact businesses, according to the 2024 Fortune/Deloitte CEO survey. The global super elections year could also impact regulations and climate policy across the globe, which in turn may influence companies’ appetites for investment as well as customer demand for clean technologies.

- Falling interest rates: Further rate cuts expected from the Federal Reserve could fuel increased investment and business spending, including on clean technology products.

- Higher costs: The demand for clean technologies is driven in part by a “green premium” some customers are willing to pay, in addition to regulatory requirements for emissions. With costs likely to remain high for industrial product manufacturers in 2025, they may need to pass on these costs to customers, which could make a green premium even more difficult for customers to justify. On the other hand, although costs remain high, they may stabilize in 2025 if inflation remains in check. This could provide an opportunity for manufacturers to reduce prices and, consequently, the green premium that customers are asked to pay.

Given these factors, companies will likely continue making cautious, targeted investments in manufacturing clean technology products that can maximize profitability and help customers meet their net-zero targets.

Tackling familiar challenges in 2025 with targeted innovation

In 2025, the manufacturing industry is likely to face familiar challenges. However, there are new approaches and tools that can be leveraged across the business to maximize efficiency, build resilience, and prepare for a potential new era of industry expansion. In fact, an optimistic scenario in Deloitte’s third quarter 2024 US economic forecast outlines the potential for an uptick in productivity and accelerated gross domestic product growth over the next several years due in part to technology investment. To position themselves as leaders in the market, manufacturers might consider taking advantage of targeted investments in their digital and data foundation, advanced technologies, and high-ROI use cases, such as:

- Advanced talent planning and management tools that can support a skills-based approach, lead to better retention, and build a workforce for the future

- AI and generative AI to enhance customer service, retain the knowledge of retirees, and bring new products to market faster

- Supply chain digitalization and tools like AI for advanced analytics and value chain simulation

- Smart operations use cases such as leveraging extended reality for efficient workforce training or customer support

- Technologies like the model-based enterprise that can support seamless collaboration with new partners and customers, which may be necessary to bring innovative low-emission products to market

Source: https://www2.deloitte.com/us/en/insights/industry/manufacturing/manufacturing-industry-outlook.html